10 Year Home Loan Calculator

10 Year Home Loan Calculator

This calculator defaults to a 10-year loan term and figures monthly mortgage payments based on the principal amount borrowed, the length of the loan and the annual interest rate. This calculator will also figure your total monthly mortgage payment which will include your property tax, property insurance and PMI payments. Then, once you have computed the monthly payment, click on the "Create Amortization Schedule" button to create a report you can print out.

For your convenience current Fairfield 10-year mortgage rates are published below.

Current 10-Year Fairfield Mortgage Rates

We publish current Fairfield mortgage rates. CT homebuyers and refinancers can use the filters at the top of the table to see the monthly payments and rates availble for their loans.

Know When a 10-Year Fixed Mortgage Can Work for You

Securing the right home loan will help you maximize your purchase. But with so many payment terms to choose from, it might be hard to know which one suits you. So before jumping into a real estate deal, it’s important to understand your options.

The most common mortgage term is a 30-year payment duration. Others take 15-year terms. Then, there are short mortgage terms that only run for 10 years. Now and then, homebuyers obtain a 10-year fixed-rate mortgage. But if you’re familiar with real estate trends, it’s not what most homebuyers usually take.

Here, you’ll learn more about the 10-year fixed-rate mortgage and what it is normally used for. With this guide, we hope you will better determine if a 10-year fixed mortgage is right for you.

What is a 10-year Fixed Mortgage?

A 10-year fixed-rate mortgage is paid with an interest rate that does not change for 10 years. In this option, you are required to pay the same loan amount every month (that’s excluding taxes and insurance, which might change over the term). Ten-year fixed mortgages usually have lower rates compared to longer terms. However, they are characterized with larger monthly payments compared to 30-year loans.

Furthermore, 10-year fixed terms are found in conventional housing loans. Conventional loans are a kind of home financing that is not directly backed by government funding. Instead these loans are provided by private lenders such as banks, credit unions, and mortgage companies - which then securitize many of the loans into MBS that trade liquidly due to backing by Fannie Mae and Freddie Mac. Conventional mortgages are taken by around two-thirds of homebuyers in America. Conventional mortgages are well-suited for people with high credit scores (no lower than 650) and a stable source of funds.

Private Mortgage Insurance

Conventional loans require a private mortgage insurance if you pay a downpayment of less than 20 percent of the home’s purchase price. This monthly insurance premium allows buyers to qualify for a loan they might not be able to get. This means it increases the cost of your loan. However, the good news is PMI is automatically terminated once your mortgage balance reaches 78 percent of your home’s price. PMI is also cancelled if you are halfway through amortizing your loan.

Ten-year fixed home loans follow a traditional amortizing schedule. Amortizing schedules are based on your monthly payments, interest rate, and loan term. It shows a breakdown of your principal and interest payments.

- Principal – The loan principal is the amount you borrowed from a lender. Also referred to as the outstanding balance, it reflects how much you still need to pay off.

- Interest – This interest is the amount your mortgage lender charges to service your loan. More interest is generated the longer it takes for you to pay a loan back.

With a regular amortizing loan, a larger portion of your payment goes toward the interest rather than the principle in the first couple of years. Then, toward the latter years (usually after 5 years), more of the payments are applied to the principal while the interest decreases.

After the agreed 10-year term, the home loan should be completely paid off. To generate an amortization schedule for a 10-year fixed loan, use our calculator above.

Why Do Consumers Obtain a 10-Year Fixed Mortgage?

Ten-year mortgages are taken by buyers who want to own their home in a short period of time. Many people use it to refinance from a longer term. This makes sense if you’re determined to pay down your mortgage before a major life event, such as retiring or sending your child to college. You can take advantage of a 10-year fixed home loan when interest rates are low.

Who qualifies for a 10-year fixed mortgage? This option is suited for buyers who can afford higher monthly payments. These borrowers usually have a good credit rating, a reliable source of funds, and high income.

Commonly Used for Refinancing Borrowers usually use 10-year mortgages to refinance to a lower rate. It allows you to pay off your loan sooner compared to a 30-year fixed mortgage.

Paying down a mortgage with a 10-year term provides homebuyers with two major benefits:

- Allows you to save thousands of dollars on interest costs

- Lets you build home equity a lot faster

For example, let’s compare a 30-year fixed mortgage and a 10-year fixed mortgage with a lower rate. The table below shows how much you can save on total interest costs.

| Loan | 30-Year Fixed Mortgage | 10-Year Fixed Mortgage | Difference |

|---|---|---|---|

| Interest rate (APR) | 3.8% | 3.25% | 0.55% |

| Monthly payment | $1,164.89 | $1,756.67 | $591.78 |

| Total interest | $169,361.62 | $66,200.95 | $103,160.67 |

Upon reviewing the costs, you’ll spend $591.78 more on monthly payments if you get a 10-year fixed rate option. However, you will save a total of $103,160.67 in interest charges with the 10-year term. It allows you to cut more than half of the interest costs.

On the other hand, many may not afford a larger loan with 10-year term. Buyers who cannot make large monthly payments typically opt for longer terms. Hence, they choose a 30-year fixed mortgage to borrow a larger amount with more affordable monthly payments.

Other Options for Refinancing Apart from a 10-year fixed home loan, if you want to refinance to a shorter term, you may also consider a 15-year fixed mortgage. Meanwhile, other buyers who need to borrow a large amount but don’t intend to keep the home choose an adjustable-rate mortgage (ARM). This is because ARMs come with a low rate and monthly payments during the first few years of the loan. Thereafter, the buyer may opt to sell the home in a couple of years.

The Pros and Cons of Taking a 10-Year Fixed Mortgage

Obtaining a 10-year mortgage is beneficial for people who can afford high monthly payments. It’s also a great option if you want to refinance to a shorter term. It enables you to own the home sooner and pay down your debt faster. However, it also comes with unique disadvantages.

You take a risk when you make larger monthly payments. It limits your purchasing power, which can be a major problem if you’re faced with emergencies in the next 10 years. With the following pros and cons in mind, consider whether a 10-year fixed mortgage can work for you:

| Pros | Cons |

|---|---|

| 10-year terms usually have lower interest rates compared to 30-year terms – may be around 0.25% to 1% lower | You may not qualify for the expensive term, requires good credit rating and high income |

| If you pay less than 20 percent down payment, it has lower mortgage insurance premium (MIP) compared to a 30-year fixed term | Larger monthly payments compared to 30-year terms |

| Since rates are locked, you don’t need to worry about increasing payments | Limits purchasing power – less cash for savings or emergencies |

| Lets you pay off your mortgage in a shorter length of time | Becomes riskier if you’re faced with a costly medical emergency or sudden job loss |

| Save more money on interest charges with a shorter term | Keeps you from making other lucrative investments |

| Lets you build equity at a faster rate – own the home sooner | Equity is tied up in your house – to use the money, you have to sell the house or obtain a home equity loan |

How Popular are 10-Year Fixed-Rate Home Loans?

A 10-year fixed mortgage is not the most common loan purchase tool for homebuyers. It’s more popular for refinancing, which is when buyers get a new loan to take advantage of lower rates. Moreover, a more popular refinancing option is a 15-year term.

Why is it uncommon? The large monthly payments make it unattractive to consumers, especially for lower income borrowers. Borrowers also need enough funds and high credit rating to refinance to a 10-year fixed term. But for those who have the money and want to pay their loan sooner, this is a good deal.

Important Notes on Refinancing

To qualify for refinancing, borrowers need a credit score of 620 to 680. But a 740 credit score will get you more favorable rates. Because of this, mortgage refinancing obliges you to improve your credit score before application.

Moreover, refinancing can cost between 2 percent to 6 percent of your loan. To justify this expensive cost, financial experts traditionally recommend refinancing when rates decrease by 2 percentage points. This ensures you reap full benefits of refinancing.

Like most loans, a shorter term entails higher monthly payments. Thus, it makes 10-year mortgages unpopular to most first-time homebuyers. Shorter loans are more suited for homebuyers with higher income and good credit scores. Meanwhile, buyers with low credit standing (and anyone on a tight budget) usually opt for a 30-year mortgage. The longer term typically has lower monthly payments. However, it also means spending more on overall interest.

Common Mortgage Terms Taken by Homebuyers

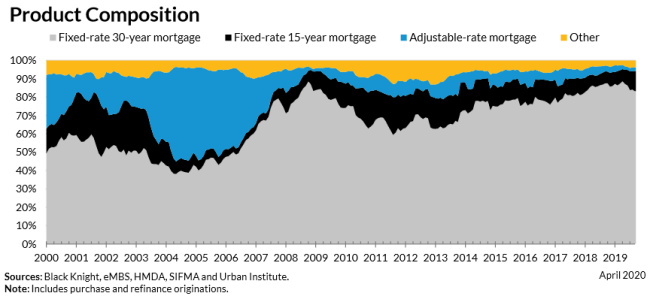

The 30-year fixed-rate loan remains the most popular type of U.S. home financing. Based on data from the Urban Institute, 30-year fixed mortgages accounted for 77 percent of new home loans in April 2020. This figure is taken from their June 2020 Housing Finance at a Glance: Monthly Chartbook.

Below is a graph from the Urban Institute showing a historical U.S. mortgage product composition and refinance share from 2000 to April 2020.

Based on the graph above, you’ll notice how 30-year fixed-rate mortgages have dominated the market for 20 years. Prior to 2009, this was trailed by adjustable-rate mortgages (ARM). But after the 2008 subprime mortgage crisis, ARMs were overtaken by 15-year fixed rate terms. This is followed by “other” types of mortgage terms such as 25, 20, and 10-year options.

Meanwhile, the 15-year fixed-rate mortgage represented 14.2 percent of new home loan originations in April 2020. More often, 15-year fixed-rate terms are used for refinancing. Refinancing is secured by homeowners who want to replace their existing mortgage with completely new loan that has more favorable terms (e.g. lower interest rate, shift to ARM or fixed-rate, etc.).

For example, homeowners refinance their 30-year FHA mortgage to a 15-year fixed-rate conventional loan. This shortens the loan term while eliminating costly annual mortgage insurance premium (MIP). They get rid of MIP while saving on interest costs. Likewise, a borrower can refinance a 30-year conventional mortgage into a shorter 10-year term.

Consumers Refinance When Rates are Low Since interest rates have dropped in late 2018, Urban Institute notes a great increase in refinance shares. It mentions government-sponsored enterprise (GSE) refinances were between 75 to 77 percent, while Ginnie Mae refinances were at 53.4 percent in April 2020.

On the other hand, adjustable-rate mortgages (ARM) accounted for 2.7 percent of home loan originations in April 2020. ARMs or variable-rate loans have interest rates that change throughout the life of the loan. It adjusts periodically when the index rate rises or decreases.

ARMs usually begin with a low rate, which adjusts after the introductory period. For example, if you have a 5/1 ARM, the rate stands for the first 5 years, after which it adjusts annually. Since interest rates may increase, borrowers must factor in the possibility of paying more. This is why ARMs are more appropriate for borrowers with higher income and good credit rating.

Furthermore, based on the data above, around 6.1 percent of loan originations accounted for other mortgage options in April 2020. This includes 25-year fixed terms, 20-year fixed terms, and 10-year fixed mortgages. It shows how 10-year fixed mortgages does not represent a huge fraction of the housing market.

Mortgage Calculations

People who commit to making mortgage payments for any length of time must understand how real estate contracts work. To stay on top of your finances, you must review your amortization schedule.

An amortization schedule is a table that shows every monetary you must make transaction each month. It tells you how much your monthly payment is based on your rate and loan term. More importantly, it breaks down how many payments you must make to fully amortize your loan in the agreed term. Meanwhile, in the case of adjustable rate mortgages, the annual interest rate may shift up or down by a set percentage.

With each 30 day period, the interest and principal balance is reduced. Thus, every payment you make takes you one step closer to paying off your mortgage.

Other Payment Factors in Monthly Mortgage Payments

Mortgage payments are not a borrowed sum that is simply repaid by a borrower. Apart from your amortized loan, there are other payment factors such as real estate taxes and annual homeowner’s insurance. There’s also private mortgage insurance (PMI) for conventional loans and mortgage insurance premium (MIP) for FHA loans. You also need to consider if the loan has fixed rate or an adjustable status, as well as the APR or interest rate.

The mortgage payment itself can be divided into two parts: the principal and interest, the regular, taxes and insurance charge. These four figures make up the total monthly payment. They may change slightly over the years depending on the type of mortgage you obtain.

Know Your PITI All these payments factors combined are referred to as PITI – the Principal, Interest, Taxes and Insurance. This figure is the true sum total of your monthly payment. PITI fluctuates over time until it is gradually paid off.

Loan Amortization

Different types of loans amortize in varied ways. For a traditional amortizing loan, a borrower must make consistent monthly payments until the mortgage is paid down in the agreed duration Meanwhile, in an interest-only loan for example, the borrower pays for the interest in the first five or 10 years of the term. Once the interest-only payment period is through, the principal remains. At this point, a borrower must make a balloon payment to pay off the remaining principal with a lump sum.

Traditional amortizing loans are more common among borrowers. Here, most of the payments go toward the interest during the first few years of the loan. Afterwards, during the latter years of the mortgage, majority of the payments go towards reducing the principal.

Make Extra Payments to Save If you are able to make extra payments toward your principal, it will reduce it faster. This helps shorten your loan term, helping you save on interest charges. But first, contact your lender and ask about any prepayment penalty you might incur. It’s best to avoid penalty fees before you pay off your loan early.

Need to generate an amortization schedule? Make mortgage computations easily by using our calculator above.

The following table shows the amortization on a 10-year $250,000 home loan at 2.8% APR for a loan that begins next year. On this example loan, payments being on August 31, 2026 for a loan originated on July 31, 2026.

You can generate a similar printable table using the above calculator by clicking on the [Inline Schedule] button. If you would like to print out your amortization schedule please click on the [Printable Schedule] button.

| Payment # | Date | Payment | Principal | Interest | Balance |

|---|---|---|---|---|---|

| 1 | Aug 31, 2026 | $2,391.01 | $1,807.68 | $583.33 | $248,192.32 |

| 2 | Sep 30, 2026 | $2,391.01 | $1,811.89 | $579.12 | $246,380.43 |

| 3 | Oct 31, 2026 | $2,391.01 | $1,816.12 | $574.89 | $244,564.31 |

| 4 | Nov 30, 2026 | $2,391.01 | $1,820.36 | $570.65 | $242,743.95 |

| 5 | Dec 31, 2026 | $2,391.01 | $1,824.61 | $566.40 | $240,919.34 |

| Year 2026 | $11,955.05 | $9,080.66 | $2,874.39 | $240,919.34 | |

| 6 | Jan 31, 2027 | $2,391.01 | $1,828.86 | $562.15 | $239,090.48 |

| 7 | Feb 28, 2027 | $2,391.01 | $1,833.13 | $557.88 | $237,257.35 |

| 8 | Mar 31, 2027 | $2,391.01 | $1,837.41 | $553.60 | $235,419.94 |

| 9 | Apr 30, 2027 | $2,391.01 | $1,841.70 | $549.31 | $233,578.24 |

| 10 | May 31, 2027 | $2,391.01 | $1,845.99 | $545.02 | $231,732.25 |

| 11 | Jun 30, 2027 | $2,391.01 | $1,850.30 | $540.71 | $229,881.95 |

| 12 | Jul 31, 2027 | $2,391.01 | $1,854.62 | $536.39 | $228,027.33 |

| 13 | Aug 31, 2027 | $2,391.01 | $1,858.95 | $532.06 | $226,168.38 |

| 14 | Sep 30, 2027 | $2,391.01 | $1,863.28 | $527.73 | $224,305.10 |

| 15 | Oct 31, 2027 | $2,391.01 | $1,867.63 | $523.38 | $222,437.47 |

| 16 | Nov 30, 2027 | $2,391.01 | $1,871.99 | $519.02 | $220,565.48 |

| 17 | Dec 31, 2027 | $2,391.01 | $1,876.36 | $514.65 | $218,689.12 |

| Year 2027 | $28,692.12 | $22,230.22 | $6,461.90 | $218,689.12 | |

| 18 | Jan 31, 2028 | $2,391.01 | $1,880.74 | $510.27 | $216,808.38 |

| 19 | Feb 28, 2028 | $2,391.01 | $1,885.12 | $505.89 | $214,923.26 |

| 20 | Mar 31, 2028 | $2,391.01 | $1,889.52 | $501.49 | $213,033.74 |

| 21 | Apr 30, 2028 | $2,391.01 | $1,893.93 | $497.08 | $211,139.81 |

| 22 | May 31, 2028 | $2,391.01 | $1,898.35 | $492.66 | $209,241.46 |

| 23 | Jun 30, 2028 | $2,391.01 | $1,902.78 | $488.23 | $207,338.68 |

| 24 | Jul 31, 2028 | $2,391.01 | $1,907.22 | $483.79 | $205,431.46 |

| 25 | Aug 31, 2028 | $2,391.01 | $1,911.67 | $479.34 | $203,519.79 |

| 26 | Sep 30, 2028 | $2,391.01 | $1,916.13 | $474.88 | $201,603.66 |

| 27 | Oct 31, 2028 | $2,391.01 | $1,920.60 | $470.41 | $199,683.06 |

| 28 | Nov 30, 2028 | $2,391.01 | $1,925.08 | $465.93 | $197,757.98 |

| 29 | Dec 31, 2028 | $2,391.01 | $1,929.57 | $461.44 | $195,828.41 |

| Year 2028 | $28,692.12 | $22,860.71 | $5,831.41 | $195,828.41 | |

| 30 | Jan 31, 2029 | $2,391.01 | $1,934.08 | $456.93 | $193,894.33 |

| 31 | Feb 28, 2029 | $2,391.01 | $1,938.59 | $452.42 | $191,955.74 |

| 32 | Mar 31, 2029 | $2,391.01 | $1,943.11 | $447.90 | $190,012.63 |

| 33 | Apr 30, 2029 | $2,391.01 | $1,947.65 | $443.36 | $188,064.98 |

| 34 | May 31, 2029 | $2,391.01 | $1,952.19 | $438.82 | $186,112.79 |

| 35 | Jun 30, 2029 | $2,391.01 | $1,956.75 | $434.26 | $184,156.04 |

| 36 | Jul 31, 2029 | $2,391.01 | $1,961.31 | $429.70 | $182,194.73 |

| 37 | Aug 31, 2029 | $2,391.01 | $1,965.89 | $425.12 | $180,228.84 |

| 38 | Sep 30, 2029 | $2,391.01 | $1,970.48 | $420.53 | $178,258.36 |

| 39 | Oct 31, 2029 | $2,391.01 | $1,975.07 | $415.94 | $176,283.29 |

| 40 | Nov 30, 2029 | $2,391.01 | $1,979.68 | $411.33 | $174,303.61 |

| 41 | Dec 31, 2029 | $2,391.01 | $1,984.30 | $406.71 | $172,319.31 |

| Year 2029 | $28,692.12 | $23,509.10 | $5,183.02 | $172,319.31 | |

| 42 | Jan 31, 2030 | $2,391.01 | $1,988.93 | $402.08 | $170,330.38 |

| 43 | Feb 28, 2030 | $2,391.01 | $1,993.57 | $397.44 | $168,336.81 |

| 44 | Mar 31, 2030 | $2,391.01 | $1,998.22 | $392.79 | $166,338.59 |

| 45 | Apr 30, 2030 | $2,391.01 | $2,002.89 | $388.12 | $164,335.70 |

| 46 | May 31, 2030 | $2,391.01 | $2,007.56 | $383.45 | $162,328.14 |

| 47 | Jun 30, 2030 | $2,391.01 | $2,012.24 | $378.77 | $160,315.90 |

| 48 | Jul 31, 2030 | $2,391.01 | $2,016.94 | $374.07 | $158,298.96 |

| 49 | Aug 31, 2030 | $2,391.01 | $2,021.65 | $369.36 | $156,277.31 |

| 50 | Sep 30, 2030 | $2,391.01 | $2,026.36 | $364.65 | $154,250.95 |

| 51 | Oct 31, 2030 | $2,391.01 | $2,031.09 | $359.92 | $152,219.86 |

| 52 | Nov 30, 2030 | $2,391.01 | $2,035.83 | $355.18 | $150,184.03 |

| 53 | Dec 31, 2030 | $2,391.01 | $2,040.58 | $350.43 | $148,143.45 |

| Year 2030 | $28,692.12 | $24,175.86 | $4,516.26 | $148,143.45 | |

| 54 | Jan 31, 2031 | $2,391.01 | $2,045.34 | $345.67 | $146,098.11 |

| 55 | Feb 28, 2031 | $2,391.01 | $2,050.11 | $340.90 | $144,048.00 |

| 56 | Mar 31, 2031 | $2,391.01 | $2,054.90 | $336.11 | $141,993.10 |

| 57 | Apr 30, 2031 | $2,391.01 | $2,059.69 | $331.32 | $139,933.41 |

| 58 | May 31, 2031 | $2,391.01 | $2,064.50 | $326.51 | $137,868.91 |

| 59 | Jun 30, 2031 | $2,391.01 | $2,069.32 | $321.69 | $135,799.59 |

| 60 | Jul 31, 2031 | $2,391.01 | $2,074.14 | $316.87 | $133,725.45 |

| 61 | Aug 31, 2031 | $2,391.01 | $2,078.98 | $312.03 | $131,646.47 |

| 62 | Sep 30, 2031 | $2,391.01 | $2,083.83 | $307.18 | $129,562.64 |

| 63 | Oct 31, 2031 | $2,391.01 | $2,088.70 | $302.31 | $127,473.94 |

| 64 | Nov 30, 2031 | $2,391.01 | $2,093.57 | $297.44 | $125,380.37 |

| 65 | Dec 31, 2031 | $2,391.01 | $2,098.46 | $292.55 | $123,281.91 |

| Year 2031 | $28,692.12 | $24,861.54 | $3,830.58 | $123,281.91 | |

| 66 | Jan 31, 2032 | $2,391.01 | $2,103.35 | $287.66 | $121,178.56 |

| 67 | Feb 28, 2032 | $2,391.01 | $2,108.26 | $282.75 | $119,070.30 |

| 68 | Mar 31, 2032 | $2,391.01 | $2,113.18 | $277.83 | $116,957.12 |

| 69 | Apr 30, 2032 | $2,391.01 | $2,118.11 | $272.90 | $114,839.01 |

| 70 | May 31, 2032 | $2,391.01 | $2,123.05 | $267.96 | $112,715.96 |

| 71 | Jun 30, 2032 | $2,391.01 | $2,128.01 | $263.00 | $110,587.95 |

| 72 | Jul 31, 2032 | $2,391.01 | $2,132.97 | $258.04 | $108,454.98 |

| 73 | Aug 31, 2032 | $2,391.01 | $2,137.95 | $253.06 | $106,317.03 |

| 74 | Sep 30, 2032 | $2,391.01 | $2,142.94 | $248.07 | $104,174.09 |

| 75 | Oct 31, 2032 | $2,391.01 | $2,147.94 | $243.07 | $102,026.15 |

| 76 | Nov 30, 2032 | $2,391.01 | $2,152.95 | $238.06 | $99,873.20 |

| 77 | Dec 31, 2032 | $2,391.01 | $2,157.97 | $233.04 | $97,715.23 |

| Year 2032 | $28,692.12 | $25,566.68 | $3,125.44 | $97,715.23 | |

| 78 | Jan 31, 2033 | $2,391.01 | $2,163.01 | $228.00 | $95,552.22 |

| 79 | Feb 28, 2033 | $2,391.01 | $2,168.05 | $222.96 | $93,384.17 |

| 80 | Mar 31, 2033 | $2,391.01 | $2,173.11 | $217.90 | $91,211.06 |

| 81 | Apr 30, 2033 | $2,391.01 | $2,178.18 | $212.83 | $89,032.88 |

| 82 | May 31, 2033 | $2,391.01 | $2,183.27 | $207.74 | $86,849.61 |

| 83 | Jun 30, 2033 | $2,391.01 | $2,188.36 | $202.65 | $84,661.25 |

| 84 | Jul 31, 2033 | $2,391.01 | $2,193.47 | $197.54 | $82,467.78 |

| 85 | Aug 31, 2033 | $2,391.01 | $2,198.59 | $192.42 | $80,269.19 |

| 86 | Sep 30, 2033 | $2,391.01 | $2,203.72 | $187.29 | $78,065.47 |

| 87 | Oct 31, 2033 | $2,391.01 | $2,208.86 | $182.15 | $75,856.61 |

| 88 | Nov 30, 2033 | $2,391.01 | $2,214.01 | $177.00 | $73,642.60 |

| 89 | Dec 31, 2033 | $2,391.01 | $2,219.18 | $171.83 | $71,423.42 |

| Year 2033 | $28,692.12 | $26,291.81 | $2,400.31 | $71,423.42 | |

| 90 | Jan 31, 2034 | $2,391.01 | $2,224.36 | $166.65 | $69,199.06 |

| 91 | Feb 28, 2034 | $2,391.01 | $2,229.55 | $161.46 | $66,969.51 |

| 92 | Mar 31, 2034 | $2,391.01 | $2,234.75 | $156.26 | $64,734.76 |

| 93 | Apr 30, 2034 | $2,391.01 | $2,239.96 | $151.05 | $62,494.80 |

| 94 | May 31, 2034 | $2,391.01 | $2,245.19 | $145.82 | $60,249.61 |

| 95 | Jun 30, 2034 | $2,391.01 | $2,250.43 | $140.58 | $57,999.18 |

| 96 | Jul 31, 2034 | $2,391.01 | $2,255.68 | $135.33 | $55,743.50 |

| 97 | Aug 31, 2034 | $2,391.01 | $2,260.94 | $130.07 | $53,482.56 |

| 98 | Sep 30, 2034 | $2,391.01 | $2,266.22 | $124.79 | $51,216.34 |

| 99 | Oct 31, 2034 | $2,391.01 | $2,271.51 | $119.50 | $48,944.83 |

| 100 | Nov 30, 2034 | $2,391.01 | $2,276.81 | $114.20 | $46,668.02 |

| 101 | Dec 31, 2034 | $2,391.01 | $2,282.12 | $108.89 | $44,385.90 |

| Year 2034 | $28,692.12 | $27,037.52 | $1,654.60 | $44,385.90 | |

| 102 | Jan 31, 2035 | $2,391.01 | $2,287.44 | $103.57 | $42,098.46 |

| 103 | Feb 28, 2035 | $2,391.01 | $2,292.78 | $98.23 | $39,805.68 |

| 104 | Mar 31, 2035 | $2,391.01 | $2,298.13 | $92.88 | $37,507.55 |

| 105 | Apr 30, 2035 | $2,391.01 | $2,303.49 | $87.52 | $35,204.06 |

| 106 | May 31, 2035 | $2,391.01 | $2,308.87 | $82.14 | $32,895.19 |

| 107 | Jun 30, 2035 | $2,391.01 | $2,314.25 | $76.76 | $30,580.94 |

| 108 | Jul 31, 2035 | $2,391.01 | $2,319.65 | $71.36 | $28,261.29 |

| 109 | Aug 31, 2035 | $2,391.01 | $2,325.07 | $65.94 | $25,936.22 |

| 110 | Sep 30, 2035 | $2,391.01 | $2,330.49 | $60.52 | $23,605.73 |

| 111 | Oct 31, 2035 | $2,391.01 | $2,335.93 | $55.08 | $21,269.80 |

| 112 | Nov 30, 2035 | $2,391.01 | $2,341.38 | $49.63 | $18,928.42 |

| 113 | Dec 31, 2035 | $2,391.01 | $2,346.84 | $44.17 | $16,581.58 |

| Year 2035 | $28,692.12 | $27,804.32 | $887.80 | $16,581.58 | |

| 114 | Jan 31, 2036 | $2,391.01 | $2,352.32 | $38.69 | $14,229.26 |

| 115 | Feb 28, 2036 | $2,391.01 | $2,357.81 | $33.20 | $11,871.45 |

| 116 | Mar 31, 2036 | $2,391.01 | $2,363.31 | $27.70 | $9,508.14 |

| 117 | Apr 30, 2036 | $2,391.01 | $2,368.82 | $22.19 | $7,139.32 |

| 118 | May 31, 2036 | $2,391.01 | $2,374.35 | $16.66 | $4,764.97 |

| 119 | Jun 30, 2036 | $2,391.01 | $2,379.89 | $11.12 | $2,385.08 |

| 120 | Jul 31, 2036 | $2,390.65 | $2,385.08 | $5.57 | $0.00 |

| Year 2036 | $16,736.71 | $16,581.58 | $155.13 | $0.00 |

To Sum It Up

Ten-year fixed mortgages are ideal for homebuyers who can afford to pay down loans sooner. It allows you to gain equity at a faster rate compared to longer terms. It’s also more commonly used as a refinancing tool for buyers who want to shorten their term and shift to a lower rate. Ten-year fixed mortgages also come with lower rates compared to longer terms.

On the downside, expect 10-year fixed mortgages to come with large monthly payments. This makes them unpopular options for consumers with tight budgets and low credit scores. That said, most homebuyers usually choose 30-year fixed rate mortgage terms. Later on, when they’ve built enough income and improved their credit score, they may opt to refinance to a shorter term. As a tip, it’s best to refinance early into the loan term.