Loan Calculator

Loan Calculator

This financial planning calculator will figure a loan's regular monthly, biweekly or weekly payment and total interest paid over the duration of the loan. Full usage instructions are in the tips tab below. Our site also offer specific calculators for auto loans & mortgages.

Simply enter the amount borrowed, the loan term, the stated APR & how frequently you make payments. We will quickly return your payment amount, total interest expense, total amount repaid & the equivalent interest-only payments to show how much you would end up spending on interest if you did not pay down the balance.

Enter the loan amount in the calculator if you know how much you will finance. If you are uncertain of how much you need to borrow, you can have it automatically calculated by entering any associated purchase, sales tax & application fees in the first section which appears if you expand the "Optional Advanced Data" drop down.

At the bottom of the calculator you can choose to create a share link for your calculation. We also provide the ability to create an inline amortization table below the calculator, or a printer friendly amortization table in a new window. Our site also offer specific calculators for auto loans & mortgages.

Current Columbus Personal Loan Rates

We publish current Columbus personal loan rates to help borrowers compare rates they are offered with current market conditions and connect borrowers with lenders offering competitive rates.

The Complete Consumer Guide to Personal Loans

Published: April 20, 2024

Credit Drives The American Economy

Standards of living are tied to consumers' ability to earn an income & borrow money for purchases they cannot make with cash on hand. Lending allowing families to own homes and vehicles they can't afford to pay for upfront is an essential economic feature, generating billions in interest payments annually while keeping money circulating through the economy. If you have a car or home loan; or even a credit card, for that matter, the amount you pay back each month reflects principal and interest payments applied toward the cost of purchases. The above calculator provides monthly payment estimates for any type of financing, breaking payments down into their essential components: principal and interest.

Interest and Principal

Before borrowing for big-ticket items, consumers establish track records of creditworthiness, using sound revolving credit histories and other successful financial transactions to illustrate their ability to meet their obligations. Income, job stability, savings and other factors are also used to bolster credit ratings, providing additional comfort for lenders while allowing trustworthy borrowers to receive funding at lower rates. As you seek funding for property, vehicles, personal costs, business start-ups and other expenses, you'll be required to lay your cards on the table, showing lenders a snapshot of your borrowing history. The financing offers & rates you receive reflect their view of information provided by credit bureaus and other reporting agencies. Once cards or other revolving credit lines are issued, basic monthly principal payments and interest depend on the terms and conditions contained within your individual cardholder agreement. While interest rates are tied to indicators like the prime rate, each card carries its own terms.

Good credit stems for several factors, each outlined on your most recent credit report. The numbers of cards you use regularly, as well as those which remain mostly idle, are considered alongside average balances and missed-payment histories. Mortgages, car loans and other personal loans are also considered when determining your credit score.

Installment and Revolving Credit Payments

Installment credit represents borrowing usually associated with the two major purchases concerning consumers: Homes and vehicles. Repayment terms vary, according to lender terms and how much money is borrowed, but monthly payments always contain interest obligations. Each installment also contains a contribution toward repaying principal, which is based on loan size and amortization schedule. From the moment you initiate your installment loan, it is possible to look at a comprehensive payment schedule, outlining your repayment obligations over the course of the loan's life. If your financing is structured using fixed rates then the schedule only changes if you pay ahead, which is allowed under some installment contracts. In other words, there are no surprises for consumers, who know exactly what their monthly home mortgage payments and vehicle loan obligations will be.

Revolving credit is a more open-ended arrangement, allowing purchases to be made on an ongoing basis. Credit cards are the most widely used form of revolving credit, providing grace periods for customers to pay back money borrowed, without interest. After a certain period of time, interest begins to accumulate and principal balances roll over into subsequent billing periods. Unlike installment payments, monthly revolving credit is based on spending activity occurring during the billing cycle. Basic interest calculator helps track monthly interest payments, clearly illustrating which portion of your revolving credit payment is applied toward reducing your principal balance.

The Consumer's Guide to Personal Loans

Applying for a personal loan is probably one of the easiest ways to secure additional cash on-hand, making it ideal for paying off credit card debt & consolidating other high-interest debt.

Application can be a bit time-consuming, which is why it is important to prepare all of the necessary documents beforehand to speed up the approval process.

What are the requirements I need to secure for my application?

The following are the common requirements that lenders look for:

- Income and employment-related documents

- Credit score reports

- Identification documents

- Bank statements

- Collateral (for secured loans)

Lenders will want to make sure that applicants are capable of fulfilling their obligations, and one way to reduce the risk of non-payment & fraud is to ensure of this is by securing documents that show proof of income/employment.

Credit score reports and bank statements are also an important for approval since this illustrates whether applicants have a good repayment history & is a good risk.

Some kinds of loans such as mortgages and auto loans are secured by the title on the property. Lenders can also use other assets to secure financing, lowering their risk & giving consumers lower rates.

How long does the approval process usually take?

The length of the approval process will depend on the lender type. For credit unions and banks, the approval process can take anywhere between a few days to a few weeks. Banks normally have stricter loan processes and higher approval standards than nonbank lenders.

If applicants opt to lend from peer-to-peer lenders, loans can get approved within a few minutes up to a few business days. Approvals tend to be faster if the applicant has already prepared all of the needed documents and other information beforehand. Repeat borrowers are likely to be approved quickly if they repaid on time during previous loans.

Online direct lenders tend to have the fastest processing periods. The application process usually takes a few minutes, and if applicants submit all of the needed documents, financing can be approved almost immediately.

What are the standard interest rates for personal loans?

Actual interest rates will vary depending on an applicant’s credit score, repayment history, income sources and the lender’s own standards. Interest rates also vary with market conditions, but for 2019 the interest rates for personal credit ranges from about 6% to 36%.

If we compare the average interest rate of personal loans to other forms of financing, we can see they have rates below that of a credit card, though charge a bit more than most secured forms of financing. The big benefits of personal loans for those who take them is they are unsecured and the approval type is typically faster than other forms of financing.

| Financing Type | Upfront Fees | APR | Benefits | Approval Time | Type |

|---|---|---|---|---|---|

| personal loans with good to excellent credit | 1% to 8% | 10.3% to 15.5% | flexible terms does not require collateral |

1 to 7 business days | unsecured, fixed |

| personal loans with bad credit | 1% to 8% | 28.5% to 32% | flexible terms does not require collateral |

1 to 7 business days | unsecured, fixed |

| credit cards | $0 to $500 | 14.6% to 25.4% | easy to use online rewards points one-month grace period |

minutes to a couple business days | unsecured, revolving |

| 5 year auto loan with good credit | $0 | 3.6% to 5% | rates locked in for duration of loan lower rates than many other forms of financing due to being secured |

1 day to 1 week | secured, fixed |

| 5 year auto loan with bad credit | $0 | 14% to 16% | rates locked in for duration of loan | 1 day to 1 week | secured, fixed |

| 30-year mortgage | 2% to 5% | 3.7% | rates locked in for duration of loan | 30-60 days | secured, fixed |

| 15-year mortgage | 2% to 5% | 3.1% | rates locked in for duration of loan | 30-60 days | secured, fixed |

| 5/1 ARM | 2% to 5% | 3.9% | lower upfront rates | 30-60 days | secured, fixed |

| heloc | $0 to $1,000 | 7.5% | works like a credit card you only pay interest if you use it |

15-45 days | secured, revolving |

| home equity loan | 2% to 5% | 6.4% | you get a lump sum upfront | 15-45 days | secured, fixed |

Credit score ratings

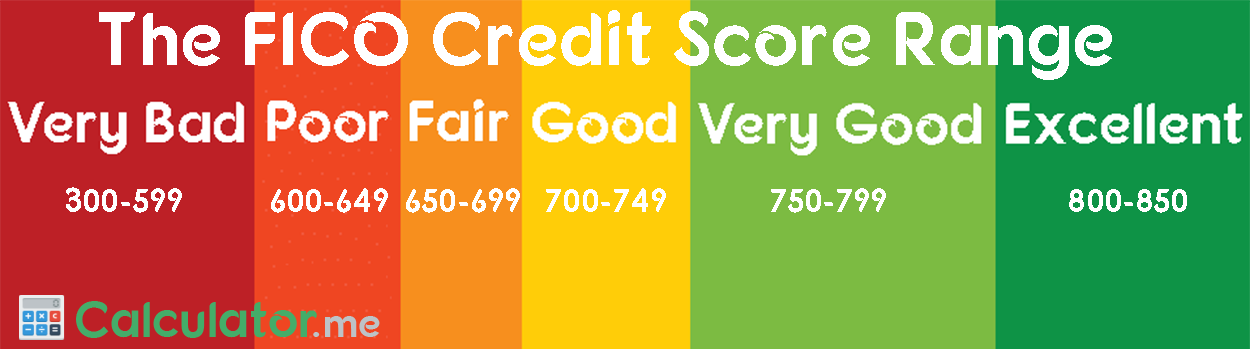

Credit score ratings may vary depending on the standard and the industry since there are industry-specific scores and several standard scores utilized across different markets. The most popular scores are FICO® Scores and VantageScore.

According to FICO® Scores, a credit rating above 800 is tagged as Excellent, 750-799 credit scores are Very Good, 700-749 scores are Good, 650-699 is Fair, 600-649 is Poor, and 300-599 is Very Bad.

If an applicant has a poor score , then the applicant will either receive a loan rejection from the lender or be required to pay an upfront fee or a significantly higher rate to qualify for financing.

Applicants whose score falls below Fair are usually considered as subprime borrowers by lending institutions.

Credit scores under the Good category are generally safe from rejections, while individuals with a rating of Very Good usually receive lower loan rates from lenders. Lastly, applicants that fall under the Exceptional category receive the best borrowing rates.

VantageScore ratings use almost the same ratings as FICO® Scores albeit with minor differences in the scoring range. A score of 781-850 is tagged as Excellent, 661-780 fall under the Good category, 601-660 is tagged as Fair, 500-600 is Poor, and 300-499 fall under Very Poor.

VantageScore Components

Applicants with Very Poor VantageScore rating will most definitely have their applications rejected, while those that fall under the Poor category will have to make do with disadvantageous rates and possibly bigger down payments.

If an applicant has a Fair VantageScore rating , their loans can get approved although not at ideal rates. Good scorers can enjoy competitive lending rates, while Excellent scorers will have the best rates and the most convenient loan terms.

How does credit score impact interest rates?

Credit scores are an indication of how well an individual has handled their debt repayments and other related finances over time, which then projects the likelihood of the applicant paying their outstanding loans on time.

Lenders will use these as basis for how low or how high the interest rates for every applicant will be.

This is why applicants with low credit risk usually enjoy lower interest rates, while those with high credit risk will have to put up with higher interest rates if not have their applications completely rejected.

When should I get a personal loan?

Since it’s so easy to get a personal loan these days, it can be tempting to use personal loans on just about anything that will require a large sum of money. However, keep in mind that multiple loans might lead one to accumulate excessive debt, which is why personal loans ideally should only be used for the following purposes:

- Debt consolidation

- Student loan refinancing

- Credit score improvement

- Emergencies

Debt consolidation

Individuals who have multiple high-interest debts can take out a personal loan to consolidate all payments into a singular monthly payment. Personal loans will usually have lower interest rates than the existing debt, making paying off debts faster.

Student loan refinancing

Personal loans can also be used for student loan refinancing purposes. Student loans usually have high interest rates ranging from 6% and up, and using a personal loan to pay off student loans will translate to lower interest rates and faster debt repayments.

However, keep in mind that this will come with certain pitfalls. This can be anything from losing the tax advantages attributed to having an existing student loan to losing benefits like deferment and forbearance.

Credit score improvement

Having mixed loans is a good way to improve your credit score, and taking out a personal loan can help in diversifying debts especially if your debt stems from a single category, such as credit cards.

Personal loans can also increase an individual’s total credit limit since it helps decrease the credit utilization ratio.

When should I use other loan options?

Other loan options, such as credit cards, mortgages, home equity loans and other secured loans are used for purposes that are unique to the nature of the loan itself.

Credit cards are the most popular form of consumer financing as they can be approved quickly & are used for virtually anything, from daily purchases to mid-scale purchases such as phones to large-scale purchases like furniture. Bonus points & the one-month grace period provide further incentives for those who pay off their balances monthly. Consumers who roll over a balance from month to month pay hefty interest fees. Those who miss payments may see their rates jump while other fees are added to their account and/or their credit line is reduced.

NOTE: If you know you will be able to pay your credit card off in full & are unlikely to roll over a balance it is a great form of short-term financing. If you carry a balance from month to month & accumulate debt with interest charges then other forms of financing may be a better choice.

Auto loans typically charge fairly low rates as it is quite easy for lenders to reposess vehicles if the borrower fails to pay their obligations.

Mortgages and equity loans are usually utilized specifically for home purchases and other large projects like home improvements which can be expensive to pay for using any other form of financing that charges higher interest rates. Mortgage rates tend to follow movements of the 10-year United States Treasury. Mortgage borrowers with a limited downpayment will likely be forced to pay for property mortgage insurance (PMI).

Best online personal loan providers

Top online personal loan providers in the US market include:

- Marcus by Goldman Sachs

- SoFi

- Lending Club

- Prosper

Marcus by Goldman Sachs

Marcus by Goldman Sachs currently has highly-competitive interest rates at 5.99% APR to 28.99% APR for non-New York residents and 5.99% APR to 24.99% APR for New York residents, with payment terms ranging from 36 months to 72 months.

Marcus is also well-known for its five-minute application process and no-fee guarantee. This guarantee includes zero fees for late payments, originations and pre-payments.

SoFi

Social Finance or SoFi is probably the best personal loan option for young professionals since it providers tools for loan repayments and services such as life insurance and wealth management. SoFi also does not charge personal loan fees aside from interest.

In addition, SoFi has a unique unemployment protection tool that makes for a useful fall back in the event of sudden unemployment on behalf of the user.

LendingClub

![]()

Although LendingClub has suffered from controversy in recent years, it has remained a top lender and is currently the largest marketplace lender.

LendingClub is famous for its loan limit amounting to $40,000, with funding getting approved and credited in just three days. Its interest rates range from 6.95% APR to 35.89% APR.

Prosper Marketplace

![]()

Prosper was founded in 2005 by Chris Larsen & John Witchel, making it the first online peer-to-peer lending marketplace. On November 24, 2008 the SEC found Prosper to be in violation of the Securities Act of 1933, but the company quickly gained a license and re-opened their site to new investors on July 13, 2009. After registering with the SEC Prosper tightened their lending criteria, choosing to focus on consumers with good credit.

Previously lenders could set the credit terms, which led to many higher rate & higher risk loans to people with weak credit scores.

Other Online Providers

Multiple other lenders have built strong online peer-to-peer marketplaces.

- Peerform allows prime & near-prime borrowers to borrow from accredited high net worth & institutional investors. Upstart, FreedomPlus, Credible & Earnest also offer personal loans.

- SunTrust's LightStream specialized in automotive loans for borrowers with weak credit profiles, but has since broadened their offering to include personal loans.

- People with poor credit scores may have to rely on payday lenders & other high-interest providers like Avant, OneMain Financial or Mariner Finance.

- Some payment processors like Paypal & Square offer loans based on the historical payment processing history associated with the business. Other companies that specialize in lending to small businesses include OnDeck Capital

- In the United Kingdom Zopa is a leading player offering personal loans with competition from companies like RateSetter & LendingCrowd. UK small businesses often borrow from the Funding Circle marketplace. Business owners who are property rich can leverage their equity using Folk2Folk while people with other valuable assets can leverage fine arts, watches & other goods to borrow securely on Unbolted. UK citizens with poor credit scores may have to borrower from companies like Wonga if they are in dire need of funds.

- Most established markets have local peer-to-peer marketplaces offering personal loans online. For example, Wisr & SocietyOne both serve Australia while Harmoney serves New Zealand & Australia. Rocket Internet founded Lendico, which serves much of Europe along with South Africa & Brazil.

- In emerging markets small businesses can enjoy low or no interest loans from charities like Kiva or Lendwithcare.

Best banks for personal loans

Three popular choices in the US market include:

- PNC Bank

- Wells Fargo

- Citizens Bank

PNC Bank

PNC Bank is one of the few banks that offer both secured and unsecured personal loans. This means that the bank caters to both individuals with high credit scores and those who have lesser-than-stellar credit scores.

Their interest rates will depend on the applicant’s current location although PNC Bank’s APR ranges from 4.99% to 19.99%. Applications can also be made either via phone, in person, or online.

Wells Fargo

Wells Fargo has personal loans ranging from $3,000 to $100,000, making it one of the banks with the widest loan ranges around. In addition, the bank also has a secured personal loan option that uses collateral for applicants that have low credit scores.

Citizens Bank

![]()

Citizens Bank’s personal loan process is probably one of the fastest among its peers since funds can be made available in as early as two days. The bank also does not charge any additional fees for personal loans.

However, Citizens Bank has a stringent application process since it only caters to individuals with high credit scores and with an income of at least $24,000.

Industry Growth Statistics

The industry has experienced an exponential growth of 269% during the last five years.

Currently, the outstanding balance for personal loans in the US market is at a 13-year high of $138 billion.

Outstanding Personal Loan Balance in the United States ($ Billions)

Source: AnnaMaria Andriotis & Peter Rudegeair, "Lenders Shunned Risky Personal Loans. Now They're Competing for Them", The Wall Street Journal, August 24, 2018, Experian

Market research data also shows that personal loans may be the easiest unsecured credit line since its requirements and approval processes are less stringent, with the industry seeing more approvals in the past couple years. The Federal Reserve conducted an economic well-being study in 2016 where they showed the types of credit households relied on after being rejected for a credit card.

| Credit Type | Percent Who Used it |

|---|---|

| Credit card | 33% |

| Personal loan from friends or family | 30% |

| Personal loans | 25% |

| Mortgage (new home) | 18% |

| Home equity loan or line of credit | 17% |

| Vehicle loan | 14% |

| Student loan | 14% |

| Mortgage refinancing | 10% |

| Other sources of financing | 18% |

In the above survey respondents could select more than one category. After trying a credit card personal loans were the next two options in the survey & the popularity of personal loans has only grown over the past couple years.

According to the Wall Street Journal in 2019 lenders started sending more personal loan direct mail pieces than credit card application mail pieces.

In the first half of this year, lenders mailed a record 1.26 billion solicitations for these loans, according to market-research firm Competiscan. The second quarter marked the first period that lenders mailed out more offers for personal loans than credit cards, a much bigger market, according to research firm Mintel Comperemedia.

Dan Behar took out a $7,000 personal loan from American Express about two years ago to help pay for a move from Long Island to Brooklyn. He still owes a few thousand dollars on the loan and has to make car and student-loan payments. He gets roughly one offer a day in his mailbox from lenders encouraging him to borrow more.

Applying for a personal loan can be time-consuming and having a good credit score is definitely an advantage, but being aware of other personal loan options that will cater to your current credit score will help you secure a loan with the most convenient payment terms as possible.